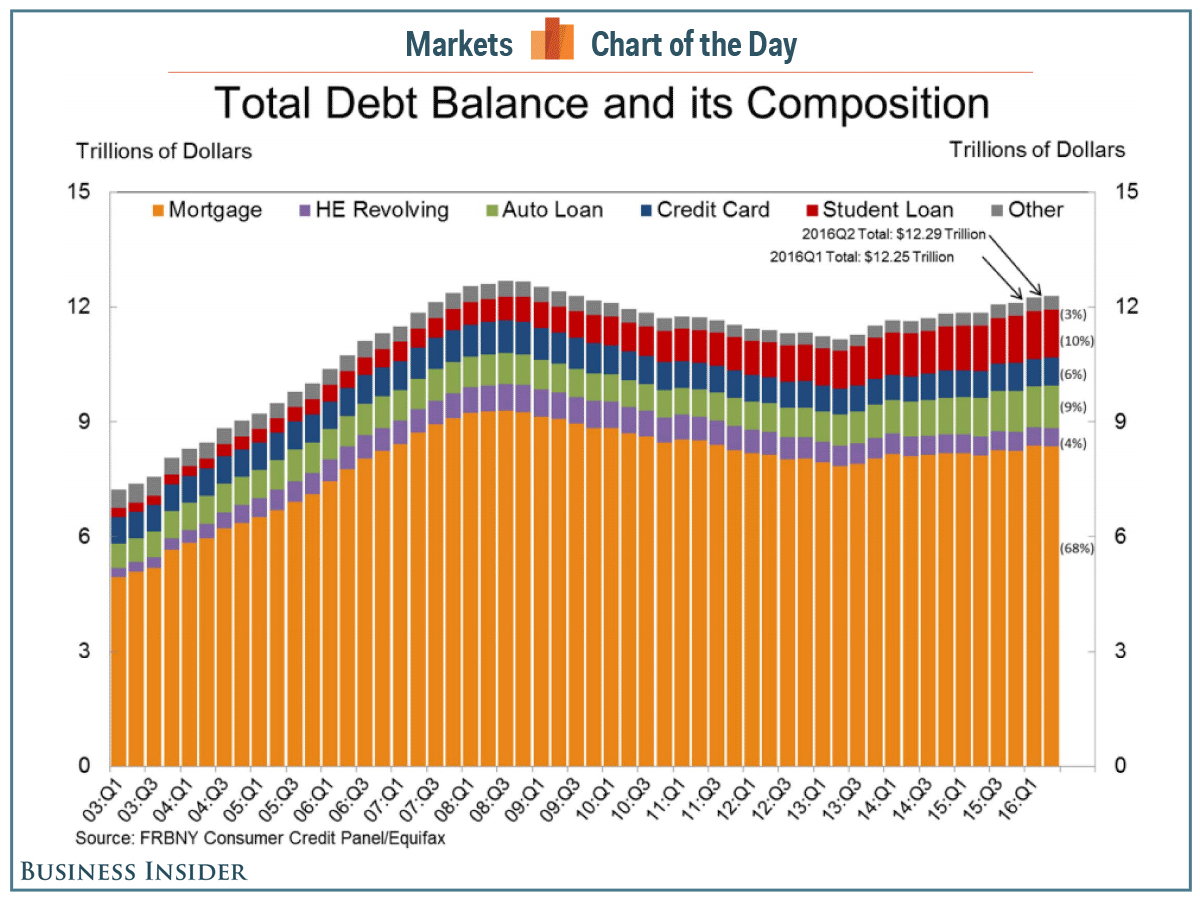

The New York Fed recently announced that U.S. household debt has ticked up again. Small percentages but still big numbers. More worrisome is the type of debt responsible for the increase:

Household debt — which includes things as varied as mortgages and credit cards — increased to $12.29 trillion in the second quarter of 2016, an increase of $35 billion, or 0.3%, according to the Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit.

“Overall household debt remains 3.1% below its 2008 Q3 peak of $12.68 trillion, but is now 10.2% above the 2013Q2 trough,” the report said.

The biggest increases came from auto debt and credit-card debt, which ticked up by $32 billion and $17 billion.

Mortgage debt actually decreased. While student loan debt didn’t go anywhere, a look at the Business Insider chart confirms all the talk: it’s a long-term troublespot.

In theory (though painful experience says it ain’t necessarily so), mortgages and student loans are “good” debt — investments in the future. Credit card debt and auto loans are “bad” debt — debt on assets that have already depreciated or non-assets (like vacations, weddings, and nights out on the town) that have disappeared altogether.

Of course, whether debts are “good” or “bad” is subjective. Some of us here would consider even modest mortgage debt a curse, while you’ll find people on various credit forums who claim bragging rights for owing $50,000 or $70,000 or more on a luxury car. Depends on your priorities, your income, your personal wish-lists, your assets, your comfort with risk, your ability and willingness to repay, how the particular debt benefits or burdens you, and probably a thousand other factors.

Something to worry about

One of the most worrisome things about the growing national household debt is that — shades of the pre-crash — a lot of it’s being run up by people who are least likely to pay it back.

For years, subprime and ridiculously long-term auto loans for people with dubious credit have been a rumbling scandal, threatening to break through surface of the financial world. Now we learn that the largest uptick in credit card acquisition is by the borrowers with the lowest credit scores.

This might not mean much, since those are also the people most likely to have lost their cards in 2008 and beyond. Maybe they’re just recouping. The low-score cohort might also include some young people breaking into the credit world, who’ll use their new cards well and build better financial reputations for themselves. So far, there’s no renewed consumer debt panic. Default rates on credit cards aren’t skyrocketing. No reason to run screaming in the streets in alarm. So far.

Nevertheless, the growth of “bad” debt, among the financially weak, in an economy that’s still staggering … well, that just can’t be a good sign.

All this got me to thinking that it’s time to revisit the question of debt among We the (More-or-Less) Prepared. Are any of us slipping into the debt trap? Everybody who’s been there knows how much easier it is to get in than out. Are we doing okay but maybe need a personal financial tune-up? Have we come up with brilliantly workable strategies for staying out of debt and building up durable assets? How will any problematic indebtedness of our friends, relatives, and neighbors affect us if (when) things go south again?

It’s not a new subject hereabouts, but it’s one we haven’t touched on in a while. I’d like to come back to that in Part II, probably a bit later this week.

I’ve always been an advocate of paying down debt. Living debt-free moved me further towards living freedom than any other change I’ve made.

People talk to me. Folks ask me about money, gold, stocks, business investments, etc.

In the past few years there has been a very marked increase in freedomistas paying off debt. I get questions about which debts to pay down first. I get messages out of the blue from people I met years ago, thanking me and telling me how great it is to be debt free.

My message to pay off debt hasn’t changed, but there are lot more people interested in it than there used to be. The fed data cited at the head of this article shows a continuing pay-down of mortgage debt. Given the insanely low interest rates presently offered on 15- and 30-year fixed rate mortgages, I find that a very encouraging sign.

There are certainly some out there who are struggling. I began my own financial tune-up a few weeks ago, something I really should do every year.

No brilliant solutions. Save something from every paycheck. Pay down debt. Don’t buy things on credit, wait until you’ve saved enough to pay cash.

My extended family certainly has a few people living high off the current credit boom. They will be hurting in the coming bust. I don’t expect that to impact me directly. In a TEOTWAWKI scenario I’ve resigned myself to admitting a few laggards; it just isn’t in me to turn hungry pre-teens away even if their parents are morons. But that doesn’t extend to debt; if they dig that hole, it is up to them to fill it.

Another reason mortgage debt is down is that home ownership is down.

http://www.realclearmarkets.com/articles/2016/08/10/homeownership_dips_to_lowest_rate_since_1960_102298.html

I owe no man. Among the top few best things I’ve done is go debt free. An important “intangible” is that it affords one a wide latitude to take risks in career, business and life. I quit my job once and got a huge raise out of the deal.

The rich ruleth over the poor, and the borrower is servant to the lender.

– Proverbs 22:7

It’s true that home ownership is down, but it’s more complicated. While the linked article notes that percentage of home ownership is down, the total number of homes owned is up. There were 115 million households in 2014, 103 million in 2000, 53 million in 1960. Using the “ownership” figures in the article, that works out to about 72 million homes in 2014 versus 32.5 million in 1960.

Several other factors tend to increase total mortgage debt. Size and cost of homes is up, term of loans is longer, and loan-to-value is up from 80% to a whopping 97.5%. That means the average “homeowner” has 2.5% equity in their home – the bank holds the rest.

All of those factors should be pushing the total dollar amount of mortgage debt up. Yet it is down from the 2008 peak, although rising the past couple years.

That abysmal loan-to-value ratio leads me to wonder if strong hands (freedomistas and others who are properly concerned about debt) have paid off their mortgages, which removes them from the charts. Those who are left are increasingly mirror-foggers and “no-nos,” (no money down, no closing costs) and others with little or no equity and no skin in the game.

Another explanation for such extreme loan-to-value ratios is people who remain underwater. If the average LTV is 97.5%, there might be quite a few above 100%, meaning they owe more than the house is worth.

That abysmal loan-to-value ratio leads me to wonder if strong hands (freedomistas and others who are properly concerned about debt) have paid off their mortgages, which removes them from the charts. Those who are left are increasingly mirror-foggers and “no-nos,” (no money down, no closing costs) and others with little or no equity and no skin in the game.

Well said. So soon after 2008, it defies all sense that banks would allow so many buyers to have so little equity.

I have always hated debt (strange for someone who has spent most of his professional career in banking and financial services; or maybe not so strange when you come to think about it!); for many years the only debt I have had is mortgages, which I am trying to pay off as quickly as possible. I buy used cars and pay cash for them; I use credit cards for the convenience but always pay them in full every month. And after so many got burned in the crash of 2008 I think more people are coming to that conclusion; witness the popularity of the Dave Ramsey radio show, whose entire mantra is being debt free.

Something that I think is related to this topic was addressed in a Wall Street Journal article yesterday called “Are Negative Interest Rates Backfiring?” Here’s a link, but it’s behind a paywall so most people probably won’t be able to read it: http://www.wsj.com/articles/are-negative-rates-backfiring-heres-some-early-evidence-1470677642 The gist of it is that the negative interest rates which have become all the rage among European central bankers are having the opposite effect than that which the “experts” predicted. They were supposed to entice people into spending more, and going into debt, which (so the theory goes) would stimulate economic growth.* The problem is, instead of borrowing more, ordinary people are instead saving more (even if they get no interest from the banks on that savings) because the negative rates engender fear among the public rather than instilling confidence. It’s always a pleasure to see the soi disant “experts” smacked in the face by reality and unintended consequences, and in the long run people will be far better off with more personal savings.

* This, of course, is classic Keynesianism, and is both demonstrably and theoretically wrong, but it has been swallowed whole by three generations of mainstream economists who cannot fathom why it isn’t working.

For this level of stupid, look to the government.

From TheMortgageReports.com:

VA Loan : Up to 100% LTV allowed

USDA Loan : Up to 100% LTV allowed

FHA Loan : Up to 96.5% LTV allowed

Conventional Loan : Up to 97% LTV allowed (Conventional means guaranteed by Fannie Mae or Freddie Mac. )

HARP 2.0 Program aka “The Obama Refi:” Unlimited LTV

FHA Streamline Refinance: Unlimited LTV

VA Streamline Refinance: Unlimited LTV. Plus no appraisal, no verification of income, employment or credit.

USDA Streamline Refinance: Unlimited LTV

With all this “help”, it’s no surprise that beginning of the year, there were 6.4 million homes with LTVs greater than 125%: seriously underwater. That is 11.5% of all mortgages.

The same report claims 12.6 million “equity rich” properties – those with more than 50% equity. That’s 22% of all mortgages, and it jumped from 10.5 million at the end of Q3 2015. Some of that is due to money printing raising home prices, but unlike the boom years less people are cashing out that helicopter-money “equity.”

Further evidence suggesting a bimodal mortgage market, with a significant and perhaps growing fraction rapidly paying down their debts while government programs encourage and enable “owning” homes with zero or negative equity.

Almost all of my debt is medical bills. That wasn’t exactly voluntarily taken on.

Hear ya, Kent. And sorry to hear that. I’ll plan to touch on unexpected expenses in part 2.

I remember reading some time back that the mortgage market was again at risk because of the government requirement that banks and others essentially grant enough (defined by the government) loans to minorities. This obviously means a lot of people who don’t have good credit will get loans they can’t afford. I can’t say it’s a stupid policy if those promulgating it know that it buys them votes, know what the results will be, and want those results to happen. Thomas Sowell has written that the correct way to assess this issue is to look at the default rates. When one does this, he said, the default rates among blacks and whites were essentially the same (without government interference), meaning the banks were doing a good job of evaluating credit risks.

Living off in the middle of a nowhere desert meant that a Prepper lifestyle was pretty much built into daily life. 95 miles to a “real” grocery, or 240 to a “real” city. I never liked debt; I wanted my income to be mine, not the bank’s nor the VISA folks. Having most of the blue-collar skills has been a big plus.

If you can use debt as a tool, all well and good. Using a loan to buy something that can be sold for a profit is indeed a good thing. Debt as a way for a soft comfy lifestyle gets way too many folks in deep doo-doo.

Note that the repo rate on cars is rising. Student loan problems are also on the increase. Unwise decision making, quite obviously.

Restaurant sales are down; food prices are up, and I see both regular credit cards as well as EBTs used for groceries. No idea how much of the credit card debt is accumulating, but I venture it’s more than many can pay off each month.

Pardon my gloom/doom, but I figure it’s gonna get worse.

I happened upon this running debt clock; I couldn’t say how accurate it is. http://usdebtclock.org/

As Dave Ramsey always says, “Debt is dumb.”

Other than our mortgage my wife and I are debt-free. (Took about ten years to pay off my college loans and credit card debt when we were first married. My gosh did I live like a drunken sailor when I was single…) Our 2003 minivan bit the dust a few months ago so we found a 2007 model that fit our needs and paid cash. Most of my coworkers were flabbergasted that we didn’t get a brand new one. I told them I didn’t want a car payment. They nodded their heads and mumbled something about how they wish they didn’t have such payments. But, living with an older vehicle is outside the realm of their reasoning.

But as a prepper I agree; it is wise to give your own finances a hard look from time to time. The timing of this article is eery – my wife and I are doing just that. It was eye-opening to see how much our family spends at Dairy Queen each month! I really like cookie dough blizzards…

The banks, card companies, student loan companies and govt all get “free” money, $trillion dollar taxpayer-funded bailouts, interest-free loans, etc., so when my banks, loans and cards continued to defraud, harass and overcharge me I gave myself a personal homemade bailout by walking out on my $90,000 in balances and left those crooks holding the bag. Too often I think libertarians and Free Market Anarchists get too caught up trying to treat the collectivist authoritarian criminal malfeasants with the same consideration we would treat our fellow libertarians and anarchists. But that’s a mistake, because bankers and card companies and loan servicers are not principled people, they are coercive sharks and purveyors of violence. The way to deal with poisonous snakes is with buckshot. I don’t let anyone walk all over me if I can help it, and these banksters crony crapitalists deserve many swift kicks in their heads from their alleged “debtors”, scratch that, their victims.

Nicolas Leobold – “Too often I think libertarians and Free Market Anarchists get too caught up trying to treat the collectivist authoritarian criminal malfeasants with the same consideration we would treat our fellow libertarians and anarchists. But that’s a mistake, bankers and card companies and loan servicers are not principled people, they are coercive sharks and purveyors of violence.”

True, many (most?) are not principled; true, they don’t *deserve* consideration. But that doesn’t negate our responsibility to the contract we may have signed, nor will reneging on that contract enhance our personal honor. They do not force us to borrow from them, nor are we responsible for their unprincipled actions. (In fact government interference into our lives and into their _modus operandi_ may be what encouraged their believing they could act without principle in the first place.)

In looking up your website, I found this: “I believe the LP Party movement can attract pro-liberty activists and supporters who can eventually become free market anarchists from what they learn in the LP.”

I disagree. The LP does not encourage the free market OR anarchists of any persuasion; if anything, it encourages collectivist group-think by setting up a platform to v*te by, and maintaining a political comparison with other Parties. By concentrating efforts on specific issues and not the libertarian reasons behind those issues, the LP has reneged on its _raison d’être_. By adhering to a minarchist stance, it gives up the cause of freedom for the compromise of pragmatism and control – the purpose of all political parties – which has no place in libertarianism.

Pat, I utterly disagree with your comments about the Libertarian Party. The libertarian movement has many components, of which the Party is only one. But it is an important one, because it gets the word “libertarian” onto ballots every election day and thereby helps increase the visibility of the movement and spread libertarian ideas. Think tanks, scholarly papers and insular blogs can do only so much; a political party promoting the same ideas is necessary, too. And you might not like the fact that politicians run the country, but you still have to deal with it.

No one really believes that Libertarian Party candidates will achieve significant electoral victories, at least not in the foreseeable future. Whatever wins it enjoys will likely be confined to local elections (many of which are in fact nonpartisan), the odd “fusion” candidate, and the occasional defection of a major party official already in office. But incremental change is still change, and is important. Of course compromise is necessary; that’s the nature of politics. This is going to be a long battle, and expecting immediate victory is a fantasy. The progressive movement has been grinding away for over a century now, and is finally achieving many of its objectives. It will take a long time (although hopefully not a century!) to unwind them. You decry compromise as “pragmatism”, as if that’s a bad thing. But it is the only way we’ll ever be able to get our foot in the door, so to speak, and begin the long process of bringing about change. (And by the way, I know of no Libertarian running under that banner who is in it for “control” or personal power. That is ludicrous. If they really wanted power they would be running on a major party ticket. Running as an avowed Libertarian, knowing that they will almost certainly lose, is conclusive evidence that they are running on principle, not for power.)

You claim that “the LP has reneged on its raison d’être. Not true. Its raison d’être, as is that of any political party, is to win elections. It is the raison d’être of the Cato Institute and other think tanks to advance the reasons behind libertarian policies. But there will be no practical means of implementing any of those policies without the foot soldiers of the LP pushing the political machinery in that direction.

Without action, intellectual preening is utterly sterile. The LP is the only source of such action.

“And you might not like the fact that politicians run the country, but you still have to deal with it.”

Laird – I understand this. But – as I have said before, elsewhere, in other wording – unlesss we keep the goal in sight, we will forget the purpose of the fight. And it is *so easy to forget the purpose* when planning by political fiat.

“Without action, intellectual preening is utterly sterile. The LP is the only source of such action.”

The ONLY source?! What are we doing here, if not helping each other find other sources – personal sources – of action? You’re talking group-think again, and group-action. But if “official” groups are the only action on the table, we WILL lose the war – as we have been losing it for the past 240 years! (Unless you think political action has won us freedom during those years; I happen to think we were freer in 1776 than we are today.)

Elections do not win freedom, they win control – whether that is the stated intent of the LP or not. And control is both addictive and blind; the actor-politician is rarely capable of seeing where his action will lead around the next bend. He is never convinced that his intent will not make the situation better. And even when (if) he admits a legal or regulatory mistake in judgement, he forgets to go back to square-1 and start over – instead he moves forward to add another mistake onto the original one, which compounds the problem. Libertarians are no different from Republocrats when they get into office. (To think that this year’s LP candidates are libertarians at all is a laugh.)

This is really not the subject of this blog, and I shouldn’t have taken it off-topic in response to Nicolas Leobold (who apparently left the LP, ostensibly because it was NOT free enough). But maybe you should ask him what convinced him the LP was not “free market anarchist,

anarcho-capitalist and voluntaryist and even more radically pro-liberty, anti-state, anti-war and pro-free markets” enough.