Okay, getting back to that rudely truncated reader survey on debt and preparedness … the survey company was kind enough to give me a couple of free days in which I could grab the accumulated results.

Technically, I could have continued taking data after that, but I didn’t know when access would be cut off again (though I did learn I could pay $19.99 to go on surveying after that). So I made a pdf of the results and here you go:

Debt and Preparedness Survey Results as of August 14, 2016.

There’s more detail in the pdf, including graphs. But a few interesting points here. (BTW, if you have trouble reading the embedded graphics in this post, go the the pdf and zoom in as much as you need to to get details. I’m discovering that embedded graphics at the new blog aren’t clickable, at least on my browser; will have to work on that. But the embedded media should now be click-to-enlargeable.)

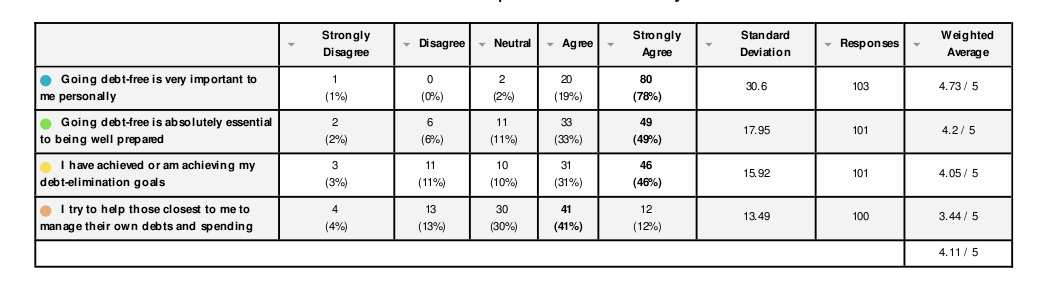

On question one, there was broad agreement, though I did notice that the later people came to the survey, the more likely they were to have divergent views:

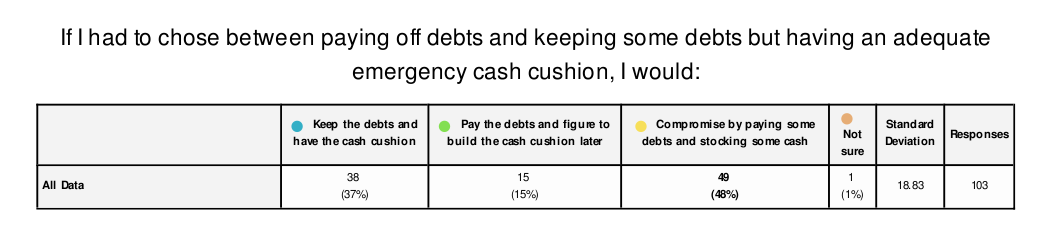

On question two, a plurality of respondents said they would compromise if faced with a choice between paying off debts and building up an emergency cash cushion, but again thoughts on that question altered as the survey went along. Initially the two most popular options ran neck-and-neck:

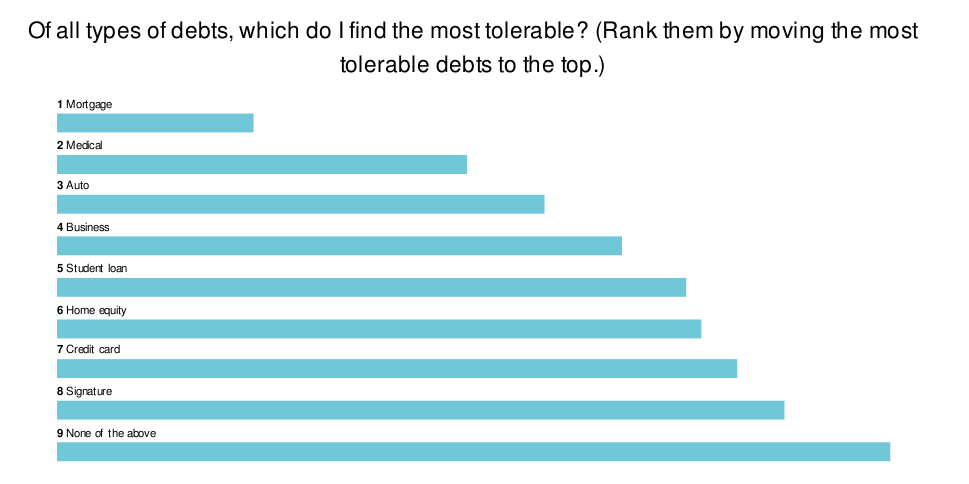

On the third question, ranking different types of debt by “most-to-least tolerable,” I at first thought people weren’t understanding the ranking process. But that was just my error of perception; I was surprised to find mortgage debt so hated — more than credit card or auto debt. But the overall judgment on that remained consistent from the first answers to the last. (I do apologize, though. I don’t think I designed this question well.) Note that in the bar chart of results, the types of debts ranked as most tolerable are at the bottom, though in the question you moved them to the top.

Question four called for text-only answers. It asked, “My biggest issue with debt and spending has always been …”

Unsurprisingly, some respondents saw the biggest problem in their own habits or happenstances while others said their biggest problem was inflicted by government. A happy few said they’d never developed any debt or spending problems. Go to the pdf to see all the answers. But here’s a sampling:

- Unexpected expenses keeping me in debt

- Working it out with my spouse

- Being afraid of running out of money-savings in my retirement

- Things, like collectibles, that I have to buy now or lose forever

- Mortgage debt; if you owe one payment or 100 you lose your house

- Tax theft leaving me less to spend or save

- Insufficient income

- My problem with spending is that I enjoy it too much!

- Poor money-management skills, wasn’t taught when I was a kid — had to learn through painful experience

Thanks to everybody who participated — and those who wanted to but didn’t get the chance. I was surprised at the enthusiastic response.

When I was answering I left question three untouched because there was no clear way to say “I don’t find _any_ debt even slightly tolerable.”

How much of this was due to personal and economic freedom in each state, I wonder?

http://www.freedominthe50states.org/overall/new-york

NY, worst state in the Union for both personal and economic freedom, also the state that had both Trump and Hillary.

> insufficient income

Sounds like something I’d write. I might have – don’t remember exactly how I responded. I’ve been under-employed for years. Well, that’s my own opinion, of course. But really, it’s just another way of stating things such as poor impulse control, and difficulty with frugality.

Off Topic: Did I miss something? Comments are CLOSED for “Tuesday links”. Is there a reason, or is that a mistake?

Pat — That was weird. Just a mistake and fixed now.

But how it happened is a mystery. Shutting off comments in WP isn’t something that can be done with just a slip of a finger (especially in this case, where I didn’t even have that option live on my post-editing screen until I put it there just now).

I can’t say I’m thrilled with WordPress these days. I liked it better when it was simpler. But then, that’s my preference for most things.