I intended to include this in last night’s post, but it didn’t quite fit.

You won’t be surprised to learn that Mssrs. Harris, McHenry & Baker, homebuilders of 1925 disapproved of renting. Sorry, renters but aside from the full page of sentimental and financial arguments they print in the back of their plan book, they go so far as to sniff at you for not exercising your full rights of citizenship.

Still, they had a point. To wit:

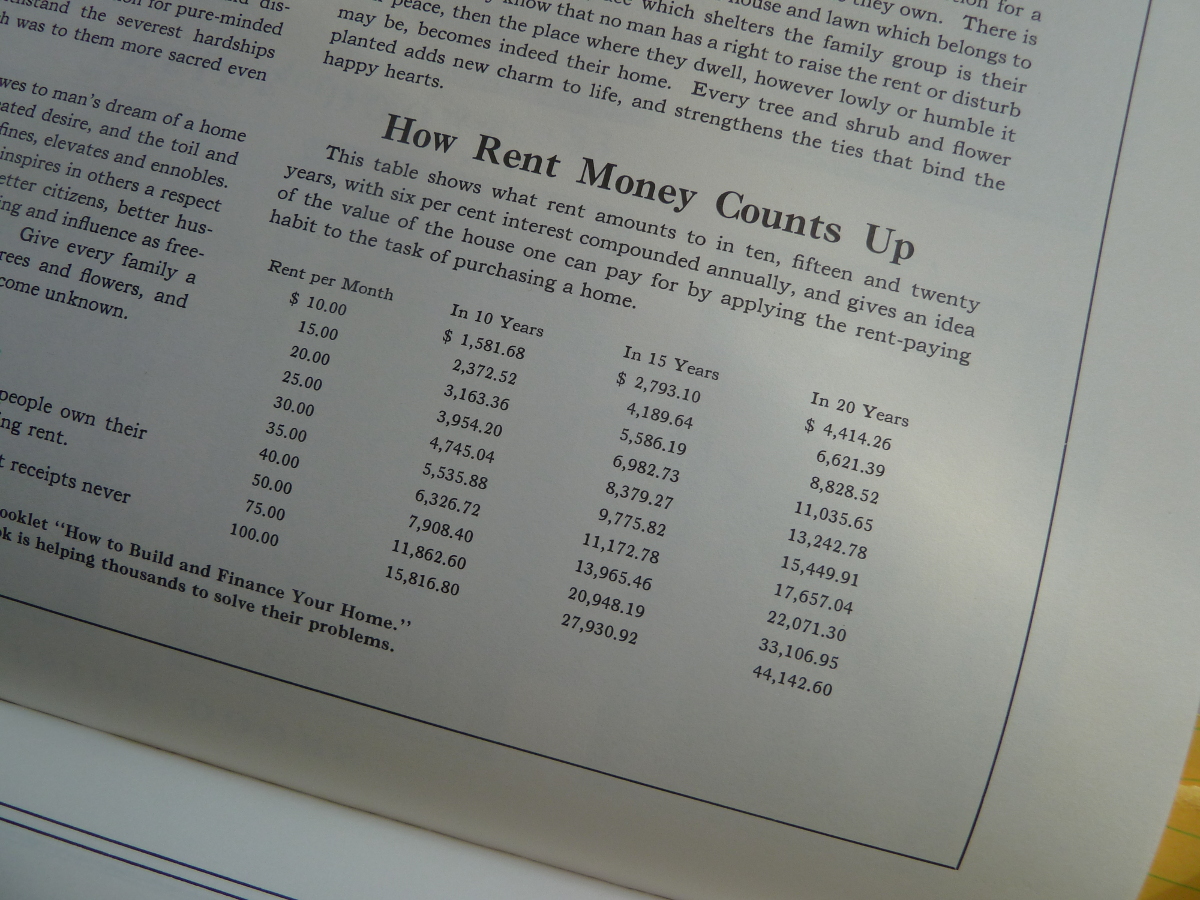

Click to embiggenate if you can’t see the figures, but they’re showing what a household’s “rent-paying habit” (yes, that’s what they call it) adds up to over 10, 15, and 20 years, assuming six percent compound interest. The low-end rent amount is $10; the highest rent they figure anyone’s paying is $100.

Granted, the average income in 1925 was just a shade over $3,000 (usually with one earner in the family), while average household income is around $60,000 now (often with two earners). And let’s not even get into why that’s so.

If we use the now-standard guideline that you can “afford” a house that costs three times your annual income, Joe and Josephine Average of 1925 could buy a $9,000 home — which was a lot of house in those days.* Now the average householder can “afford” a $180,000 home.

In my town, $180,000 could get you a slightly neglected Victorian or Craftsman on a hill with a nice view. Not a bad house, but one that needs TLC. OTOH, the local average income is far below $60k. In San Francisco, Boston, NYC, or Seattle, $180,000 wouldn’t even buy a bare, trash-covered lot, and you’d better hope you had one of the famous jobs in finance or high tech, rather than one of the jobs waiting on the high-finance-tech folks at Starbucks.

Of course all then-vs-now comparisons are bogus. There’s never a direct correspondence. The denizens of 1925 were, for instance, probably paying a much larger percentage of their income for transportation and appliances. But then, they also paid vastly lower taxes unless they were rich. In those days, more people probably saved up and paid cash for houses or at least made giant downpayments; nowadays, it’s mortgage all you can. There’s just no way to draw nice, straight lines.

So you can quibble about the figures and parse them as you like. You can have some fun calculating how far your $25 monthly rent or mortgage payment would have gone in 1925 compared with your $750 rent or mortgage payment now. You can curse the Federal Reserve and damn ever-expanding government. You can get nostalgic looking at Craftsman houses and the former costs of owning them.

Just remember that there never were any Good Old Days, and that smug and prosperous 1925 was just a whisker away from the disaster of 1929.

—–

* Shortly after the crash of 1929, my grandparents bought a large, impressive stone edifice in a good neighborhood for $2,000. The architect who built it for his own family had committed suicide and the property was what the folks of 2008 would have called distressed. In 1925, the same place would have probably cost several times more. Dollar for dollar, grandpa and grandma got a much better deal than the one I got when I bought Ye Olde Wreck for $10,000. But in both cases, an earlier homeowner had to suffer for the deal to become possible.

Having lived both kinds of life, I don’t see the often touted advantage of buying be renting – at least not while there is a mortgage.

If you calculate the TCoL (my term – total cost of lodging) all those things homeowners pay for over time need to be factored in, yet seldom seem to have been included, I’m not certain there’s much difference. Yard maintenance, new roof, painting, plumbing issues, snow removal, chimney repairs, yada yada. As a homeowner I either called someone and paid them or got the tools (mower, snow blower, etc.) and did the work myself. As a renter I called the office and somebody called somebody else and it got done.

Agreed, there are plenty of costs and PITAs with home ownership. But in the end, unless you go the mortgage-second-mortgage-HELOC route that so many did before 2008, you have an asset — probably the largest most people will ever have.

And if you have zero mortgage or a fixed-rate mortgage, you’ve also got good padding between you and inflation.

But I know renting can make a lot of sense for a lot of people. Not for me, though. I’m a nester and I like to own, despite the drawbacks.

My experience as a renter has always been that the landlord just kind of shrugs when something that isn’t property-destroying happens, and says if I want it fixed, I’m free to fix it. Half the time I’m allowed to take it off the rent, but the other half, no… “if you want that fixed you can pay for it”. “Owning” a house, at least I don’t have to plead to get something fixed (if I can afford it).

A friend of mine got into a fight with his landlord over a dangerously damaged wood stove chimney. The landlord refused to fix it, and refused to let him take the cost of repairs off his rent. So my friend stopped paying rent and lived, in winter weather that ranged from around 10 to -40 degrees, in this house with no heat and no running water. He slept in one of those “100 below” sleeping bags, inside a pup tent, in his bedroom. And refused all invitations to visit me, just across the river, because he didn’t want to get used to heat. This feud lasted 6 months or more and my friend eventually moved away.

This feud lasted 6 months or more and my friend eventually moved away.

Holy cr*p. Your friend is either amazingly principled or almost fatally stubborn. Or both. Couldn’t he have fixed the chimney, then taken the landlord to court to force him to pay?

Something I’ve never understood: the idea that it’s advantageous to rent or lease (special circumstances aside, of course). Supposedly, the rule of thumb is that if the value of something is going to decrease in time, you should rent or lease it (cars, for example), and if it will go up (land, for instance), you should buy. Well, let’s take cars. Every car has an owner. And if those commercial owners who offer cars for lease aren’t making the lessor pay for the car’s depreciation, then that owner is stupid — and I doubt that they are. And the owner is going to make a profit on the lease, and that has to be underwritten by the lessor, too. So … I don’t get it.

Then there’s my own practice: buy ’em ten to fifteen years old, drive ’em carefully, and keep driving until the cost of a repair that I can’t do myself exceeds the cost of replacing the beater with something similar. It’s worked fairly well for me, and besides, it appeals to my cheap, cheap nature. I hate to get rid of anything before it’s really, truly, and completely used up!

Back in 1908 when my Great Grandparents bought the family home, they paid $50 down and $5 bucks a month until their $750 was paid off. I have the bill of sale from that.Mind you I grew up in that house until my parents sold it for $17000 in 1974.

Back in 1977-84 I did construction projects for the VA. In seven years, we moved six times. I really wanted to rent, but there was simply nothing decent available. That was Fayetteville, Arkansas; Poplar Bluff, Missouri; Lebanon, Pennsylvania; Grand Island, Nebraska; Amarillo and San Antonio, Texas. Buying homes in that situation is not fun.

Earlier, 1969-1977, we did rent. Out of five homes/apartments/duplexes, one landlord was really interested in maintaining the property. That I do not understand.

OTOH, we’ve been here for 30+ years, and owning has been great.

Lessons:

1. You never pay off a home. You can pay the mortgage, but there’s still insurance and taxes.

2. Short-term, a home really shouldn’t be considered an investment, in that you need one. As my wife says, “It isn’t an investment until you can sell it.” Yes, homes often appreciate in “value.” But so do the homes you have to replace it with if you sell it. That equation changes somewhat when you get to the stage of downsizing.

I’ve always figured that renting just means I’m paying someone else’s mortgage and building an asset for them. So I’ve hated renting. My wife always considered renting “cliff dwelling” and she never really felt at ‘home’ unless she owned it, so she hated renting, too. There is a pride of ownership/stewardship of a piece of property and a home. It doesn’t need to be new, or fancy, or impressive, but it needs to be MINE.

I think there is more than a sales pitch in those promotional materials. There’s also the kernel of truth.

Here in NH, if there’s a faulty issue involving safety, the landlord is NOT ALLOWED to charge rent. There’s a ( mostly reasonable ) list of things that a home / apartment must comply with to be allowed before it can be rented, including a working septic system, clean water, electricity, and heating.

“Couldn’t he have fixed the chimney, then taken the landlord to court to force him to pay?”

Believe it or not, he was probably even less likely than me to voluntarily go to court for anything. He was very stubborn. And a little crazy, too. But mostly a good guy.